By Legal Futures Associate Lockton

By Legal Futures Associate Lockton

The marketplace experiences two main peaks whereby a true reflection can be given as to the conditions buyers of Insurance were facing, these months being in April and October, where we estimate between 85%-90% of firms renew in these months. 2024 was a positive year from an Insurance buyers perspective, we witnessed a further dilution in respect of Insurers rate, and this accelerated as the year progressed.

There were three core factors in rate dilution, these being:

- A renewed appetite for growth from established Insurers. A number of Insurers had no intentions for growth in recent years, this approach has now shifted for some, but not all.

- New Entrants- 2024 saw the arrival of a further new entrant, this arrival coupled with those who entered in 2023 have resulted in new capacity seeking to grow portfolios and build critical mass.

- A stable claims environment- despite there continuing to be the emergence of larger losses, the market has been ventilated from a “new trend” of attritional claim. In years gone by, be it, buyer funded developments, Right to Buy, Cyber crime or escalating ground rent, the market has managed to avoid a new wave of loss.

The one caveat would be that rate reductions were not experienced for all firms, there remain pockets of the profession where there remains a reluctance from Insurers to deploy capacity, particularly:

- Firms with fees below £500,000 and a high proportion of commercial and/or residential property exposure

- Firms whereby directors/partners are at, or nearing retirement age with no succession plan in place.

- Financial Mis-selling work

We have analysed four main factors across our portfolio of circa 1,700 SRA regulated practices across 2024:

- Primary Layer rate increases – The cost of Insurance as a proportion of a law firms revenue

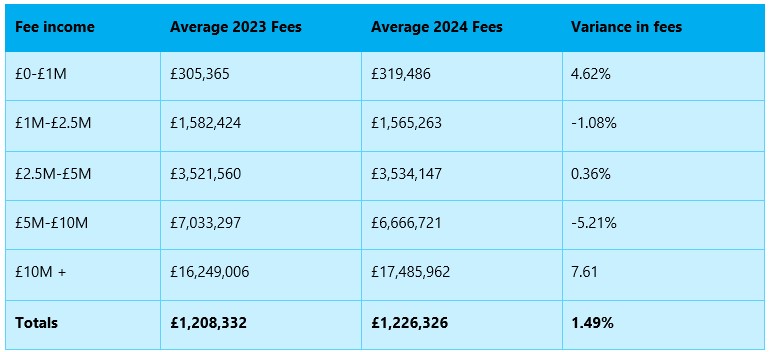

- Premium Changes – The change in total premium

- Revenue Performance of legal practices

- Excess Layer rate increases- The cost of excess layer Insurance as a proportion of law firms revenue

This data is taken from placements across the main SRA participating Insurers for over 1,700 firms. The main themes from the data show that across 2024, the average primary rates and premium have diluted once again. One item of note is that there was a slow down in the growth of average revenue, whilst growth was still apparent, the average growth has reduced somewhat from what was occurring in 2022 and 2023.

Further analysis

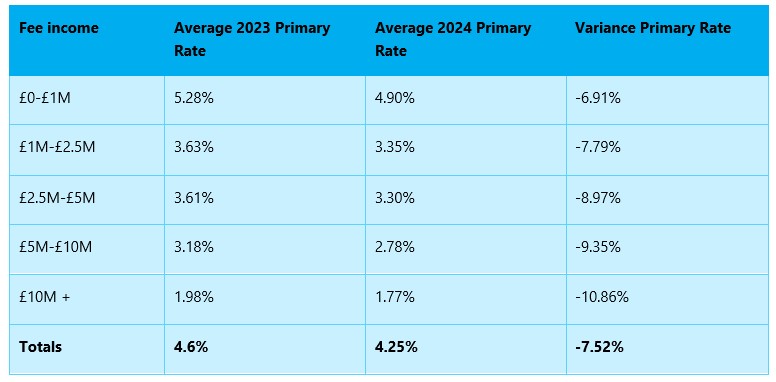

In addition to the above, across the circa 1700 firms within the Lockton portfolio, we have drilled down further in respect of primary rate, rate being the percentage of Insurance cost relative to revenue.

There are factors that will contribute to rate, and one would anticipate those firms with more exposure to higher risks areas of work and/or significant claims payments would be experiencing higher rates than the average, and those with lower risk areas of work, and/or no claims would be experiencing lower than average rates. What the analysis clearly demonstrates is the dilution of rate as a firms revenue increase, it also highlights that the rate dilution experienced in 2024 was more notable the larger a firms revenue.

2025: The outlook from an Insurers perspective

As we have touched on above, there is reason for continued optimism across 2025, primarily as a result of new entrants, and the majority of established Insurers having an increased appetite and premium targets to meet. The signs are positive, and we anticipate greater competition for a number of SRA regulated practices and the likelihood of further new capacity entering the marketplace across the next 12 months.

Whilst we have commented above around further improvements and that conditions across 2024 have been more favourable for the buying community, as we head in to 2025, there does remain concern from the Insurer community, particularly those who have Insured SRA firms for a sustained period.

Insurers have identified a number of areas that could result in issues across their portfolios, including:

- Financial health of a practice – There continues to be notable collapses of practices, such collapses can tend to bring with them significant claims

- Fraudulent Acts- There have series of high profile thefts of client account across 2024. Insurers continued to be concerned as to the rising severity when such events occur.

- Integration of AI- Insurers are embracing the role of AI, however they also wish to see firms really controlling the use of AI from the “centre”. Insurers have two main concerns, the first being firms having no clear policy for AI usage and scenarios whereby AI is being used by a minority in the business and a firms leadership being unaware AI software is being utilised. The second major concern is the lack of human verification when firms choose to use AI, Insurers do have a concern that AI software is not perfect, and it is vital that there is scrutiny of the content the AI is generating.

- AML & Identification checks – Increase in seller fraud across 2024.

- Financial Mis-Selling Work- Perhaps the most significant emerging risk to Insurers across 2024. The year saw a number of high profile collapses of firms, and in the case of some firms, the aftermath resulting in discussion and activity in Westminster. Insurers are cautious of such work, primarily due to the funding structures that are in place for such work and the risk that this prevents.

- Aggregation principle- PII Insurers continue to be concerned as to the courts application of the aggregation principle, the most recent such example being Discovery Land Vs Axis. The SRA MTC’s require Insurers to provide any one claim coverage, the challenge this presents to Insurers is that they have no protection as to the worst possible loss scenario, their liabilities are not capped at the total limit, and in claims scenarios where the aggregation principle is being interpreted as it is currently, these claims can be extremely costly and result in a primary Insurer paying £10’s millions .