By Suzanne Shepherd, a Chartered Financial Planner with Wealth Experts, a member of Legal Futures Associate, SIFA Professional

By Suzanne Shepherd, a Chartered Financial Planner with Wealth Experts, a member of Legal Futures Associate, SIFA Professional

My client Mabel was looking for advice on Will Planning and preparing Lasting Powers of Attorney, and approached a local solicitor who I regularly work with. The solicitor was able to establish that Mabel would benefit greatly from advice in regards to her Inheritance Tax (IHT) liability, and recommended my services. As a SIFA Professional and SOLLA member, who also holds the STEP Financial Services qualification, I often advise clients in their later years with all their financial planning needs.

Mabel is currently in her late 80’s, but don’t let her age fool you- she is remarkably fit and healthy for her age! Neither I nor the referring solicitor had any concerns surrounding her capacity or capability to engage with advice throughout the planning process.

I’m always mindful that a client could potentially be in a vulnerable circumstance, and as people age, this concern increases. It’s incredibly important to me that my clients have the support they need to be able to make the best and most comfortable decisions for them and their family.

Often, the estate planning advice process involves the client’s closest family members. In this case, I asked Mabel to invite her daughter to our meeting, so that all parties who would be affected by the advice were involved from the very beginning.

Our approach

Our initial meeting was an opportunity to get to know Mabel, and gain a deeper understanding of her requirements, so I could discover what was most important to her and plan accordingly.

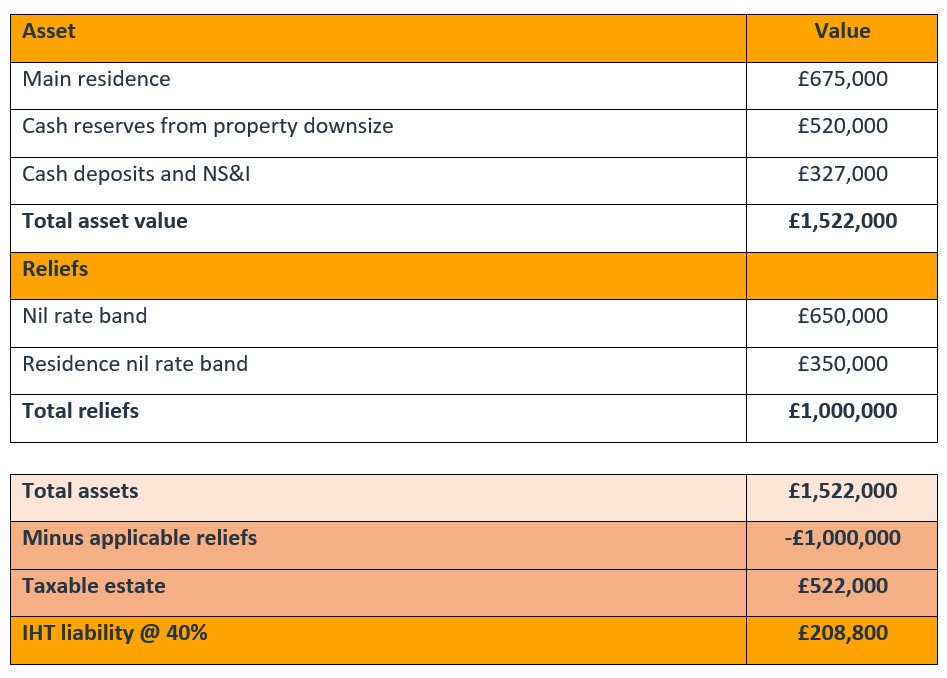

I learnt that Mabel had sold her home for £1.2 million, to downsize to a property worth around 50% of this value. In addition to the profit attained from this house sale, there were other assets involved. If Mabel were to pass away, this would mean that the beneficiaries of her estate would have to pay a large sum of IHT. Neither Mabel or her children wanted to see the families hard earned assets liable for unnecessary tax.

Mabel wanted to reduce her IHT liability, and wanted to consider the possibility of her supporting her children with their own mortgages and any outstanding debts. Mabel’s husband sadly passed away a few years prior, and as she inherited his entire estate, this means that upon her death, Mabel’s estate would benefit from double the individual nil rate band of £325,000 and the residence nil rate band of £175,000.

As Mabel is in her later years, I ensured that I was incredibly mindful when creating her plan of action, and it was paramount that the outcome would be the best possible option for Mabel.

Following our in-depth discovery discussion, I then calculated Mabel’s total assets, and applied any applicable IHT reliefs which would help to confirm the total IHT liability.

A tailored solution is the best solution

We discussed different mitigation strategies and options available to Mabel, which included life insurance, outright gifting, trusts and investments. A concern of Mabel’s was that she may not live for another 7 years. After weighing up the pros and cons of all options, I recommended using an investment that would qualify for Business Property Relief (BPR), which is equal to her taxable estate value of £522,000, as the best fit for Mabel, given her circumstances and concerns surrounding her longevity.

My recommendation would ensure that Mabel retained full access to the investment, should they ever be required. With a BPR-qualifying investment, the shares then become 100% IHT exempt after a holding period of just two years- providing the shares are still held at the time of death and remain invested within the BPR environment.

Mabel also decided to gift a total of £100,000 to her children, to help them clear their remaining mortgage payments and any personal debts. Mabel understood that these gifts would remain in her estate IHT calculation for the next 7 years, and if she passed away during this time, their value would be brought back into the IHT calculation.

Providing peace of mind for Mabel

Providing Mabel survives for a further 2 years, by accepting my recommendations, she will not leave an IHT liability for her estate beneficiaries. This not only means a potential saving of £208,800 to Mabel’s children, but they will also benefit from the targeted investment growth on the sum invested in BPR investment and will receive the potential of a moderate growth rate targeting 3% per annum.

Mabel was delighted with this outcome, and it certainly put her mind at ease to know that she was now in complete control of her assets.

As financial planners, we appreciate that nothing in life stays the same. Like all our clients, Mabel will benefit from our ongoing annual review service, and we’ll continue to review her plans and make any changes, should they be required with her best interest at heart.

This financial advisory company is listed on the SIFA Professional Directory of financial advisers (Midlands Region) – to view their details please Click Here